The Venture Capital Industry in 2009: Over/Under

With this week marking the start of the NFL season, and the calendar marching toward the fourth quarter, there’s no better time to do a bit of speculation around how this year may end up for the venture industry. Especially when you can have it take the form of the over/under wagers commonly associated with the sport (which are only made for fun of course). Half the fun was in deciding what the over/under should be the rest is in the takes. Here we go:

Category: Venture capital index return for 2009 (one year/end-to-end)

Over/Under: 6.5%

The Take: UNDER

This was a tough line to formulate without the second quarter venture capital index return which is not yet available. The Cambridge Associates US Venture Capital Index return for the first quarter was at -2.9% and the preliminary second quarter end-to-end return currently stands at 0.16%. With the NASDAQ up well over 10% in the third quarter so far, it’s fair to say the venture index will track further upward in Q3 and probably Q4. The venture index has been less volatile than the public markets despite FAS 157 mark-to-market rules, but the trend down the line should still be upward. There should be some bump in valuations before the year is out, but since exit activity will remain weak, the index should have a tough time breaking 6% for the year.

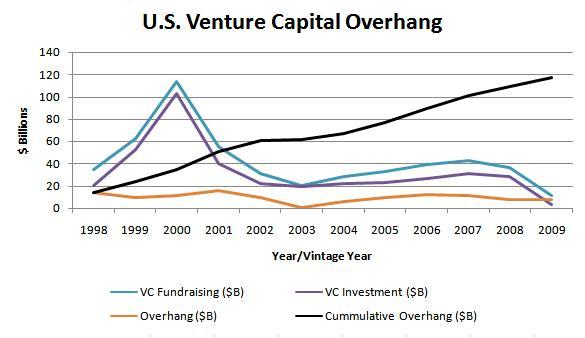

Category: Venture capital fundraising totals for 2009

Over/Under: Funds: 125, Dollar Amount: $12 Billion

The Take: UNDER – both number of funds and dollar amount

At the end of the second quarter, 70 venture capital funds had raised a total of $6.3 billion. Fundraising activity declined significantly in the second quarter, when only $1.7 billion was raised by 25 funds. As we find ourselves amidst the toughest fundraising environment in some time, limited partners have shown no signs of increasing their rate/level of commitment in the near future. Allocations within private equity for most institutional investors have either remained unchanged or dropped for venture, while increasing for more opportunistic strategies. Well established firms and proven general partners should be able to raise funds, but newer firms and those with less than stellar track records will have trouble.

Category: Venture capital deal-making totals for 2009

Over/Under: Deals: 2,750, Dollar Amount: $15.5 Billion

The Take: OVER – both number of deals and dollar amount

At the end of the second quarter, venture capitalists had invested in 1,215 deals totaling $6.9 billion. Investment activity was quite consistent between the first and second quarters. There’s the sense that investment activity has dropped a bit in the third quarter but that deal sizes seem to be larger, perhaps reflective of a shift to investment in the healthcare and cleantech sectors. Look for venture capitalists to continue to invest in innovative new companies, particularly as they should still have the upper hand on deal terms and valuations. Follow-on investments in later-stage companies will continue as well since the exit market will not open up significantly at least till next year.

Category: Total number of venture-backed IPOs in 2009

Over/Under: 9

The Take: PUSH

At the end of the second quarter there were just 5 venture-backed IPOs for the year, I’m counting just the LogMeIn and Cumberland Pharmaceuticals IPOs since, and projecting just two more. You have to have faith that two more venture-backed companies can hold an IPO in the next four months buoyed by the solid performance of those that have managed to go public so far this year. The good news is that 2010 looks to be a much better year.

Category: Total number of venture-backed M&A exits in 2009

Over/Under: 230

The Take: OVER

Through the end of the second quarter there were 121 M&A deals in which venture-backed companies were acquired. At the start of September we were at around 165. While the third quarter will probably end in line with first and second quarter totals, I’m expecting the fourth quarter to be relatively more active. The over/under is adjusted for this expectation, but I’m still taking the over. Strategic buyers, particularly those with abundant cash reserves will probably look to take advantage of depressed valuations while they last. 2010 could see a rise in valuations, especially if the IPO market opens up a bit more. It’s still worth it to note though that even if we manage to reach 300, the year will go into the books with the lowest venture-backed M&A tally since 2003.

Note: NVCA data was used for all the statistics in this post

AV

AV

{kind=link}