Should Venture Funds Consider J-Curve Mitigation Strategies?

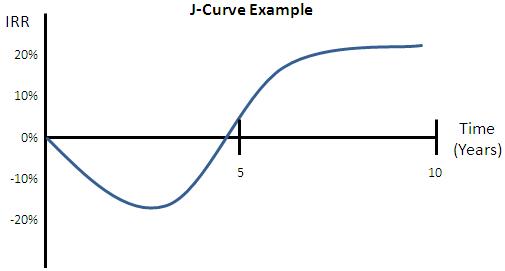

Most everyone involved with the venture industry is familiar with the J-curve. It is used to describe the nature of returns in a venture fund (based on the internal rate of return or IRR). Returns are typically negative in the early years and then turn positive in the range of three to five years after the fund starts investing. This happens as a result of a number of factors, including: management fees (which make up a larger portion of called capital early in a fund’s life), under-performing investments that are identified early and written down, and also the simple fact that investments take time to mature and grow.

All in all, for investors with a long-term focus such as those investing in venture capital, the J-curve is is not a major concern since all good funds eventually emerge from it. Unfortunately though, in evaluating venture funds some investors irrationally eschew what are quality venture funds and firms based solely on IRR since it’s the most prominently used return measure and also the most commonly benchmarked. Funds with deeper J-curves or even funds whose early returns are viewed by investors without full understanding of the J-curve are often unfairly judged. This begs the question of whether or not venture funds would well served by taking actions that mitigate the J-curve. As the industry has come under scrutiny over returns and the competition over limited partner commitments intensifies, the idea of a venture funds using j-curve mitigation tactics isn’t so farfetched.

J-curve mitigation already happens at the portfolio level of institutional investors by mixing in funds with strategies that produce more immediate cash flows. Examples include secondary funds, direct secondary funds, venture debt funds and co-investments. Let’s say a venture firm wanted to mitigate the J-curve in a fund, what tactics could they use?

- Defer management fees to later years of the fund – management fees early in the life of a fund are a major drag on the IRR. Firms that can afford to defer them to later years of the fund could mitigate the J-curve and boost IRR.

- Be less conservative with valuations – by not writing companies off early or holding companies close to cost when they can be written up, a fund could boost NAV and IRR as a result.

- Alter the fund’s early investment strategy. Examples include:

- PIPE deals – investing in publicly traded companies. The liquidity associated with the public markets means an investment could be made and turned around in a short period of time.

- Venture debt – providing debt financing to already venture-backed companies. Debt payments mean early cash flow while warrants can provide the option for future equity.

- Early late-stage deals – If a fund has a balanced strategy in terms of investment stage, concentrating late state deals early in a fund’s life would provide early liquidity to mitigate the J-curve.

- Direct secondaries – purchasing an investor’s (founders, employees or even venture funds) interest in a venture-backed company that is close to a liquidity event.

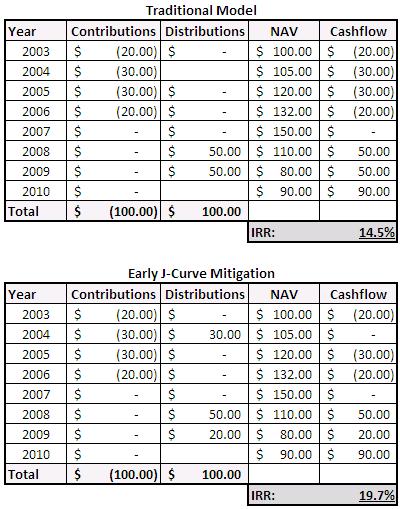

Below is an example of how early liquidity can not only help mitigate the J-curve but also impact a fund’s overall IRR. I’ve assumed that a fund is able to produce the same level of distributions regardless of strategy (the only difference being timing):

As you can see, in addition to mitigating the J-curve, IRR can be boosted significantly by providing a moderate level of early distributions. Of course the difference in return is almost purely optical since the return multiple remains the same. Furthermore, by implementing these strategies, a venture fund is almost surely forcing a strategy that might not be optimal for the team, market and long-term benefit of the fund and limited partners.

Are investors concerned enough with the J-curve that they would accept lower risk-adjusted returns to mitigate it? The right answer to this question has always been no, since most sophisticated investors realize the long-term nature of the asset class (and use a broader measures of performance including return multiples). Still, the possibility of funds implementing such strategies is more real now than ever before, as managers try to keep ahead of peers and gain any edge they can in appearing better to less informed investors.

AV

AV