Venture Capital Overhang Continues To Shrink

Before getting to the data, I’d like to share why I’m changing how I look at the overhang statistic:

I’ve been writing about the venture capital overhang (or amount of “dry powder” available) each quarter for a while now but never felt extremely confident in the figures I’ve reported. Unfortunately the overhang figure is highly subjective and I don’t think anyone except maybe a Cambridge Associates could even come close to accurately estimating how much uncalled capital is out there - the true overhang. As a proxy, I (and other publications) use the difference in reported venture capital fundraising and investment data (as reported by the NVCA, Thomson Reuters and PwC). The trouble with this methodology starts with the fact that both the fundraising and investment data sets are continuously changed retroactively - I’m guessing as funds and deals are backfilled into their databases. Furthermore, it’s unclear to me whether or not fundraising data for a certain period is later updated for capital raised by funds in that given vintage year after that year has passed. To make matters even more complicated, things like management fees, recycled capital and investment by U.S.-based firms outside of the U.S. are unaccounted for.

I’ve always said that venture capital industry data is often highly questionable, no matter the source, and that instead of focusing on absolute numbers, the focus should be on changes in the data. Because of this, and because of the issues with the fundraising and investment data, I’ve decided to focus on the near-term trends relating to the overhang, as opposing to trying to paint a larger picture.

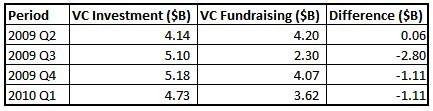

Here’s a look at differences in venture capital fundraising and investment data through the second quarter of 2010:

What clearly stands out is the huge disparity between venture investment and fundraising in the second quarter of this year. I can say pretty confidently that this is probably the largest such disparity since at least 2002, when fundraising screeched to a halt but venture firm coffers were still brimming from the fundraising boom of 2000. This time around though, there are different dynamics at play. For one, the preceding fundraising bubble was not nearly as large, meaning that we may be spared another decade-long hangover and that the industry should recover faster. But this also means that competition for survival among venture firms may be fierce.

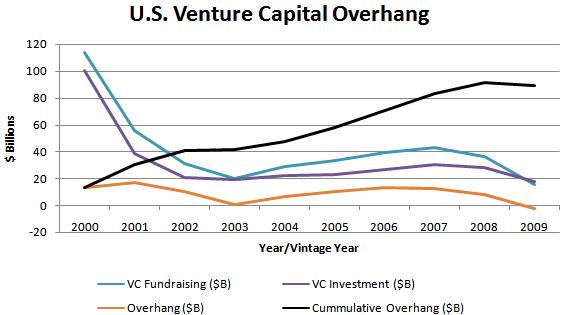

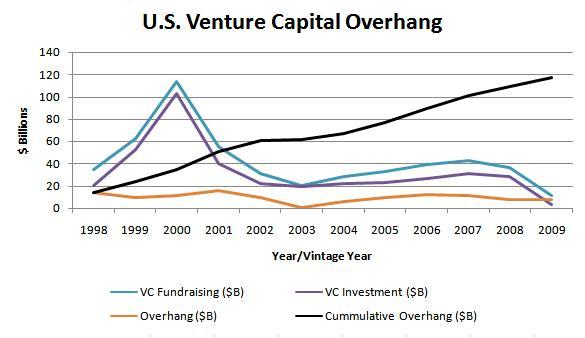

Investment can’t outpace fundraising forever. Initially I had thought that after the third quarter of 2009 we might start seeing a leveling out of the differential, but clearly I was wrong. The huge disparity in the most recent quarter shows that we may have longer to go and there may be more quarters to come with investment outpacing fundraising. This phenomenon could be thought of as sort of a market correction: fringe firms that raised funds years ago will eventually run out of capital and will be unable to raise new funds. What we should see after this “correction” is fewer firms, but higher quality firms remaining, investing in better deals at better valuations and generating better returns - not necessarily a bad thing for the industry. Something else to keep in mind is that the number of funds raising capital isn’t down as sharply as the total amounts being raised, meaning firms are raising smaller funds, which should lead to a reduction in the number and/or size of deals which also brings the industry back down to a more efficient level.

Data: The NVCA, Thomson Reuters and PwC

AV

AV