Venture Capital Overhang: Shrinking

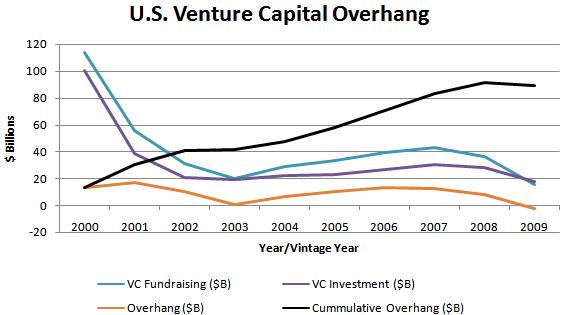

With 2009 now behind us, full final year-end venture industry data is available. There’s plenty to glean from all the fundraising, investment and exit data. Much of it tells us what we already knew or expected: fundraising and investment are down, and exits have improved, but just slightly. There’s so much you can analyze, but I’ll focus on something I’ve done in the past, which is looking at the “venture capital overhang.” This is the difference between the aggregate capital raised by venture capitalists and the amount invested. It gives us a rough idea of how much capital VCs have available for investment, sometimes referred to as “dry powder.” The chart below shows venture fundraising, investment, the difference between fundraising and investment (as the overhang) and the cumulative overhang for the last ten years.

The cumulative overhang for the last decade for the U.S. venture capital industry totals close to $90 billion, using my methodology and data from PwC, Thompson Reuters and the NVCA. As with so much of the data on the venture capital industry, the calculation is not perfect. Things like management fees and recycled capital are unaccounted for. There’s also the issue of investments made outside of the U.S. which are not captured in the PwC MoneyTree data. Rather than focusing on exact numbers, its more important to focus on trends and to look at the big picture.

For one, there’s clearly capital out there for venture capitalists to invest. It’s probably becoming more concentrated across a fewer number of firms - as I mentioned in my last post, good firms will continue to be able to raise capital. The overhang number is down from my previous calculation earlier this year, which signalz to that capital will be a bit scarcer. Going forward, we should see more years like 2009 and 2003 where the levels of investment and fundraising have less of a gap and less of an overhang is created. Now, you don’t want things going in the other direction, where we have more capital invested than raised because that would of course be unsustainable. But then some would also argue that the huge levels of overhang amassed in years past were also unsustainable, which is probably true.

There needs to be certain level of reasonability maintained in the industry and less overhang will force venture capital firms to be more prudent in deploying capital. This doesn’t mean, however, that great new ideas won’t get funded, because VCs clearly have plenty of dry powder. If anything we’ll see more early / seed stage deals which not only require less capital, but have more potential upside and also bring the industry back closer to its roots of more risk taking.

AV

AV

Reader Comments